Break-even analysis is used to examine the relationship of costs and profits to the volume of business. Break-even analysis is the most popular form of cost-volume-profit analysis. It is a technique which determines the level of operations of an organisation at which its total sales is equal to its total cost. Break-even point is that level of output where total revenue is equal to total cost. At this point, a firm has zero profit, zero loss. Above the break-even point a firm will generate profit and below the break-even point it incurs losses.

At this point:-

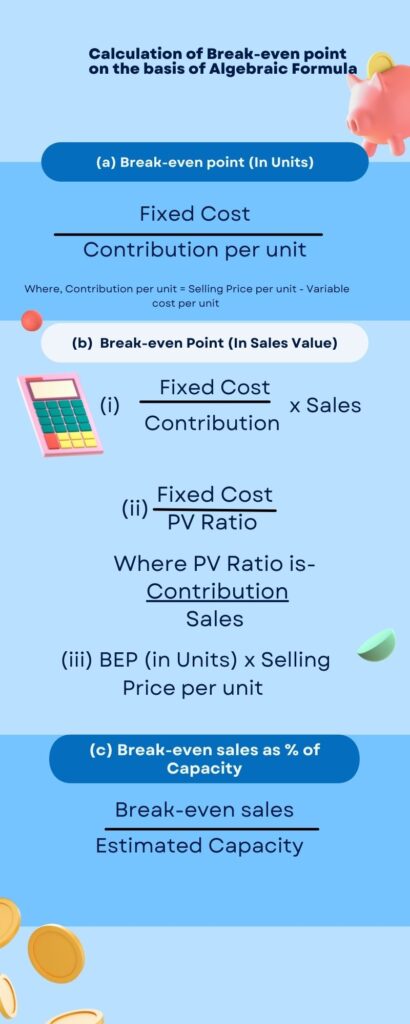

Total Revenue = Total cost So, profit= 0

Total Fixed cost = Total contribution So, profit= 0

Sales at Break-even Point = Fixed Cost + Variable Cost

Calculation of Break-Even Point on the basis of Algebraic Formula

Example

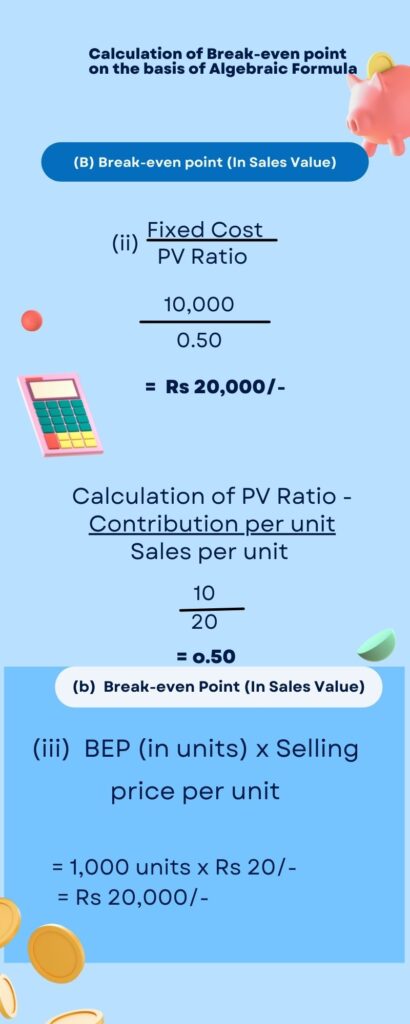

Question

Calculate break-even point in units and in sales value on the basis of the following information-

Output- 2000 units

Selling price per unit- Rs 20/-

Variable cost per unit – Rs 10/-

Fixed cost – Rs 10,000/-

Solution

Conclusion

Break-even analysis assists the management in profit planning, cost control and decision making. Lower the fixed cost lower is the break-even point. Break-even point helps the management to determine when they will start making profit. It also provides the level of operation below which a firm could not run profitably.